In June 2026, the median home sale price in Byron, GA was $293,000 across 37 closed single-family sales, with 62 single-family homes for sale and an average of 48 days on market. Here is the one-sentence read on the Byron real estate market: it is the I-75-corridor value market on the western edge of the area, where first-time and commuter buyers find approachable prices and varied housing stock, and where sellers priced more realistically in June, closing the gap to asking and moving homes faster than a month earlier.

The rest of this report breaks down what those numbers mean, where the leverage sits by price band, how today's mortgage rates and Byron's property taxes factor in, and my outlook for the months ahead. One important distinction up front: unlike Perry, Warner Robins, Bonaire, and Kathleen, the city of Byron sits in Peach County, not Houston County, so its taxes and jurisdiction work differently, which I cover in detail below.

Byron Housing Market at a Glance: June 2026

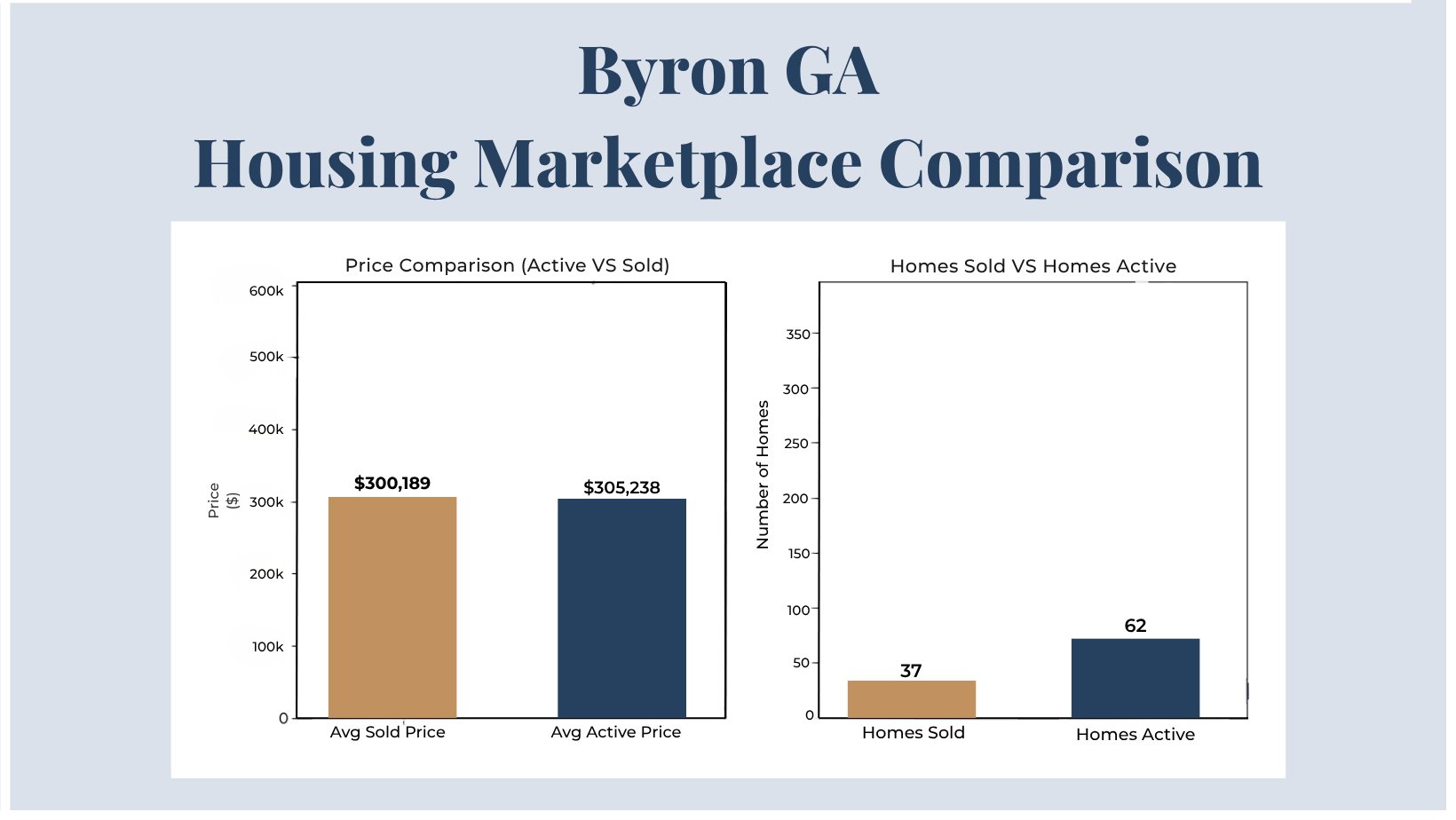

Median sale price (single-family): $293,000, essentially flat from $294,410 in May 2026

Average sale price (single-family): $300,189

Homes sold: 37 single-family (38 across all property types)

Active inventory: 62 single-family homes for sale (75 across all property types, including townhomes and manufactured and mobile homes)

Average days on market: 48 days (sold), down from 64 in May, vs 68 days (active listings)

Median asking price of active listings: $298,877, only about $5,900 above the median sold price

Market balance: roughly 1.7 active listings per sale, balanced

Bottom line: the area's affordable, I-75-corridor market where sellers got more realistic, the asking-to-sold gap narrowed, and homes sold faster

Median vs. Average Sale Price: What Byron's Prices Really Tell You

Two numbers describe Byron's prices, and they tell slightly different stories. The median sale price was $293,000, and the average was $300,189. The median is the exact midpoint of all sales, half of Byron's homes sold for more and half for less, which makes it the most reliable read on a typical home. The unusually small gap between the median and the average, only about $7,000, tells you Byron sales cluster tightly without the high-end outliers that skew other markets, which makes the $293,000 median an especially dependable benchmark.

Compared with May, the median was essentially flat, edging from $294,410 to $293,000, a change of less than one percent. That is stability. At just under $300,000, Byron sits among the more affordable markets in the area, near Perry and above Warner Robins, and that approachable median is the heart of Byron's appeal as a genuine entry point for first-time buyers, with quick Interstate 75 access for commuters heading toward Macon or the Robins Air Force Base area.

Days on Market: What 48 Days (and 68) Really Mean in Byron

Days on market measures how long a listing takes to go under contract. In Byron, homes that sold did so in an average of 48 days in June, a meaningful improvement from 64 days in May. Homes still on the market had been listed an average of 68 days, down from 77 in May. Both numbers moving lower tells you Byron's market picked up pace this month.

As a rule of thumb, a sold pace under 30 days is a hot seller's market, 30 to 60 days is balanced, and beyond 60 days favors buyers. Byron's 48-day sold pace is solidly balanced, and the improvement from 64 days is the clearest sign that Byron sellers priced more realistically in June, which got homes moving. The gap between the 48-day sold pace and the 68-day active average still shows some overpriced inventory sitting, but that gap is narrower than it was in May, a healthier picture for the market overall.

The Narrowing Gap: Asking Price vs. Sold Price in Byron

The single most useful insight in this report is the spread between what sellers are asking and what buyers are paying, and in Byron it narrowed sharply. Active listings carry a median asking price of $298,877, while homes are closing at a median of $293,000, a gap of only about $5,900, or roughly 2 percent. In May, that spread was about $23,590, so the asking-to-sold gap collapsed as the median asking price came down from $318,000 to $298,877.

That is a significant shift for a market that usually carries the widest negotiating room in the area. It tells you Byron sellers recalibrated to where homes are actually closing, and the payoff showed up in faster sales. For buyers, the practical message is that the deep, across-the-board discounts of a wide-gap market are less available this month, since inventory is now priced closer to reality, though there is still room to negotiate on individual listings that have been sitting past the 68-day active average. For sellers, June is a reminder that realistic pricing is what moves homes here.

Inventory and the Balance of Power in Byron

The clearest read on the balance of power is inventory relative to sales. There were 62 active single-family listings against 37 closed sales in June, about 1.7 homes available for every one that sold, a balanced ratio. Active single-family inventory rose from 53 in May to 62 in June, so buyers have a bit more to choose from, while sales held steady at 37 against 38 a month earlier.

Across all property types, Byron has 75 active listings and 38 recent closings, and its inventory is the most varied in the area, spanning single-family detached homes, townhomes, and manufactured and mobile homes. That range is part of what makes Byron accessible: there are genuine entry points below the single-family median, including townhomes in the $240,000s and manufactured and mobile homes lower still. For buyers seeking the widest set of affordable options, Byron offers the most varied housing stock in the market.

Where the Leverage Is by Price Band in Byron

Byron's demand is concentrated in the value bands. Most of June's closings landed between roughly $235,000 and $310,000, the heart of the first-time and commuter market, and well-priced homes in that range are the ones that moved as the 48-day sold pace improved. Buyers in this core have a solid set of options across single-family homes and townhomes, and, with the asking-to-sold gap now narrow, should focus on homes priced to recent comparables rather than expecting deep discounts everywhere.

The upper end of Byron, above roughly $400,000, is thin on both sides, with only a handful of sales and a small number of higher-priced active listings, including homes reaching into the $600,000s and one single-family attached listing near $950,000. That thinness means upper-end buyers have more leverage and more time, while sellers there face a small, selective pool and need sharp pricing. For most Byron buyers and sellers, though, the action, and the value, is in the sub-$310,000 core.

How Today's Mortgage Rates Factor Into the Byron Market

Home price is only half of affordability; the mortgage rate is the other half. As of the week of June 25, 2026, Freddie Mac reported the average 30-year fixed mortgage rate at about 6.49 percent, essentially flat from 6.47 percent the week before and down from 6.77 percent a year earlier. Rates in the mid-6 percent range have held steady for weeks, which is part of why buyers stayed active through June.

Here is what that means in dollars for a typical Byron home. On the $293,000 median with 20 percent down, financing about $234,400 at 6.49 percent over 30 years runs very roughly $1,480 a month in principal and interest, before property taxes, insurance, and any HOA dues, with a full payment landing near $1,850 to $2,000, factoring in Peach County's somewhat higher effective tax rate. Under the 28 percent rule of thumb, that points to a household income in the neighborhood of $78,000 to $85,000 to buy comfortably at the median with 20 percent down. Byron's affordability makes it a natural fit for first-time buyer programs: Georgia Dream down payment assistance, VA loans with no money down for eligible service members and veterans, FHA loans at 3.5 percent down, and USDA loans, which offer zero down in eligible rural areas that can include parts of the Byron and Peach County countryside. Comparing three to five lenders is one of the simplest ways to save.

Byron's Bigger Picture: The I-75 Corridor and Peach County

Numbers describe a single month; context explains why a market behaves the way it does. Byron sits at the Interstate 75 corridor on the western edge of the Middle Georgia market, which is the foundation of its identity: it offers approachable prices and quick highway access for commuters heading to Macon, Warner Robins, and the Robins Air Force Base area, without the price points of the Houston County suburbs. That combination of affordability and access is what draws first-time and commuter buyers.

The most important structural fact about Byron is jurisdictional: the city sits in Peach County, not Houston County. That distinction shapes its property taxes, its school district, and its local government, and it is the single most common point of confusion for buyers moving between Byron and the Houston County cities. Byron also sits near ongoing commercial and industrial growth along the I-75 corridor, which supports steady, value-oriented housing demand on the western edge of the region.

My Outlook for the Byron Market

Here is how I read Byron heading deeper into the summer, based on the June data rather than on guesswork. The encouraging signal is that sellers recalibrated. The asking-to-sold gap narrowed sharply, from about $23,590 to $5,900, and the sold pace improved from 64 days to 48, which together tell me that more realistic pricing is moving homes. The essentially flat median shows values are steady, not falling, even as pricing got sharper.

For the months ahead, I expect Byron to stay balanced and value-driven. With a bit more inventory on the market and sellers pricing closer to reality, buyers in the sub-$310,000 core have a healthy set of options without the frustration of chasing overpriced listings, and sellers who price to recent comparables should keep seeing faster sales. The upper end remains thin and buyer-friendly. For anyone weighing Byron against the Houston County cities, the Peach County tax picture is the key variable to run before deciding, and it is worth doing that math up front.

What This Means for You

If you're buying: Byron is the area's affordable, I-75-corridor value play, with the most varied housing stock, from single-family homes to townhomes to manufactured and mobile homes. This month the asking-to-sold gap narrowed, so the days of deep discounts across the board have eased, focus on homes priced to recent comparables and on any listing sitting past the 68-day active average for negotiating room. Byron's sub-$300,000 median makes it a strong fit for first-time buyer programs, VA, FHA, and USDA loans, so ask a lender which fits. One must-do before you commit: run the Peach County tax math, since it differs from the Houston County cities.

If you're selling: June proved the point: realistic pricing moves Byron homes. Sellers who brought the median asking price down closed the gap to sold prices and cut the sold pace from 64 days to 48. Price to recent comparables for your band and neighborhood rather than testing a high number, because Byron buyers are value-focused and will pass over an overpriced listing. In the sub-$310,000 core, a well-priced home in good condition should move at a healthy pace. If you are selling above $400,000, be realistic, that end of the Byron market is thin, so sharp pricing and strong presentation matter even more.

Frequently Asked Questions: The Byron, GA Housing Market

Q: What is the median home price in Byron, GA in June 2026?

A: The median single-family sale price in Byron was $293,000 in June 2026, based on 37 closed sales, essentially flat from $294,410 in May. The median is the midpoint of all sales, so half of Byron's homes sold for more and half for less. The average was close behind at $300,189, and the unusually small gap between them, about $7,000, tells you Byron sales cluster tightly without the high-end outliers that skew other markets. At just under $300,000, Byron is among the more affordable markets in the area, which anchors its appeal to first-time and commuter buyers.

Q: Is Byron, GA in Houston County or Peach County?

A: Byron is in Peach County, not Houston County. This is the single most important distinction for buyers comparing Byron to Perry, Warner Robins, Bonaire, or Kathleen, all of which are in Houston County. Because Byron sits in Peach County, its property taxes, school district, and local government all operate under Peach County rather than Houston County, so the tax math and the jurisdictional details differ. Anyone weighing Byron against the Houston County cities should confirm the Peach County specifics before deciding.

Q: Is Byron, GA a buyer's market or a seller's market right now?

A: In June 2026, Byron was balanced and improving for sellers. There were about 1.7 active listings for every sale, a balanced ratio, and the sold pace quickened to 48 days from 64 in May as sellers priced more realistically. The asking-to-sold gap narrowed sharply, from about $23,590 to $5,900, which means the deep, across-the-board negotiating room of earlier months has eased. Buyers still have leverage on individual listings that have been sitting and at the thin upper end above $400,000, but the value-band core is now more balanced than buyer-dominated.

Q: How many homes are for sale in Byron, GA?

A: As of the June 2026 report, there were 62 active single-family homes for sale in Byron and 75 across all property types, including townhomes and manufactured and mobile homes. That is up from 53 single-family listings in May, so buyers have a bit more to choose from. Byron's inventory is the most varied in the area, offering genuine entry points below the single-family median, including townhomes in the $240,000s and manufactured and mobile homes lower still, which is part of what makes it accessible to first-time buyers.

Q: What is the average days on market for homes in Byron, GA?

A: Single-family homes that sold in Byron in June 2026 did so in an average of 48 days, a solid improvement from 64 days in May. Homes still on the market had been listed an average of 68 days, down from 77 in May. As a rule of thumb, under 30 days is a hot seller's market, 30 to 60 days is balanced, and beyond 60 days favors buyers. Byron's 48-day sold pace is solidly balanced, and the improvement from May is the clearest sign that more realistic seller pricing got homes moving this month.

Q: Are homes in Byron, GA selling for over or under asking price?

A: Byron's inventory is now priced close to where homes are actually closing. The median asking price of active listings was $298,877 against a $293,000 median sold price, a gap of only about $5,900, or roughly 2 percent, which narrowed sharply from about $23,590 in May. That means the deep, across-the-board discounts of a wide-gap market are less available this month, since sellers recalibrated their pricing. There is still room to negotiate on individual listings that have been sitting past the 68-day active average, but on a well-priced home, expect to pay close to ask.

Q: Why are Byron's property taxes different from Houston County?

A: Because Byron is in Peach County, not Houston County. A Byron homeowner's bill is built from Peach County taxes, the City of Byron millage, and the Peach County school levy, rather than the Houston County and Houston County school rates that apply in Perry, Warner Robins, Bonaire, and Kathleen. Byron's effective property tax rate runs around 1.26 percent of fair market value, with a median bill in the neighborhood of $2,400, modestly higher than typical Houston County bills. Georgia's statewide rules still apply, assessment at 40 percent of fair market value and the mill-based calculation, but the specific rates and any local floating-homestead adoption are set by Peach County, so confirm your figure with the Peach County Tax Commissioner.

Q: How much are property taxes in Byron, GA?

A: Byron property taxes are based on Georgia's standard method, 40 percent of fair market value multiplied by the local millage rate, but the millage comes from Peach County, the City of Byron, and the Peach County school system rather than Houston County. The effective rate runs around 1.26 percent of fair market value, which puts the median Byron tax bill near $2,400, modestly higher than most Houston County bills. On a $293,000 home, that points to roughly $3,600 to $3,700 a year before exemptions, with homestead and other exemptions reducing it for owner-occupants. Because rates and exemptions are set locally, confirm your exact figure with the Peach County Tax Commissioner.

Q: How much income do I need to afford a home in Byron, GA?

A: A common rule of thumb is that your monthly housing payment should stay near 28 percent of your gross monthly income. On Byron's $293,000 median with 20 percent down and a 30-year fixed rate around 6.49 percent, principal and interest run very roughly $1,480 a month, and with Peach County property taxes, insurance, and any HOA dues the full payment lands near $1,850 to $2,000. That points to a household income in the neighborhood of $78,000 to $85,000 to buy comfortably at the median with 20 percent down. Zero-down VA or USDA financing can lower the cash needed up front, and your actual figure depends on your down payment, credit, and debts, so a local lender can give you a precise pre-approval.

Q: What first-time home buyer programs are available in Byron, GA?

A: Byron's affordability makes it a strong fit for first-time buyer programs. The flagship is the Georgia Dream Homeownership Program, run by the Georgia Department of Community Affairs, which pairs a below-market first mortgage with down payment assistance, generally $10,000 for standard buyers and up to $12,500 for the PEN and CHOICE categories covering public protectors, educators, healthcare workers, active military, veterans, and families with a disabled member. The assistance is a zero-interest second loan with no monthly payment, repaid only when you sell, refinance, or move out, and it generally requires a 640 credit score, a homebuyer education course, and income and purchase-price limits. Byron buyers can also use VA loans with no money down, FHA loans at 3.5 percent down, and USDA loans, which offer zero down in eligible rural areas that can include parts of the Peach County countryside. A local lender can confirm which fit.

Q: Do USDA loans work in the Byron, GA area?

A: In many cases, yes. USDA loans offer zero down payment in designated rural areas, and parts of Byron and the surrounding Peach County countryside can qualify, which is a meaningful advantage for value-focused buyers. Eligibility is tied to the specific property address and to household income limits, so a home on the rural edges of Byron may qualify while one in the denser core may not. Because Byron pairs affordability with rural-edge geography, it is one of the better local markets to explore USDA financing. Your lender can run a quick address check to confirm eligibility.

Q: What price range of homes sells best in Byron, GA?

A: The heart of Byron's market sits between roughly $235,000 and $310,000, the first-time and commuter value range where most of June's closings landed and where the improving 48-day sold pace showed up. Buyers there have a solid set of options across single-family homes and townhomes. Above roughly $400,000, Byron is thin on both sales and inventory, so upper-end buyers have more leverage and time, while sellers face a small, selective pool. For most buyers and sellers, the value and the activity are in the sub-$310,000 core.

Q: Is now a good time to buy a home in Byron, GA?

A: For value-focused and first-time buyers, Byron offers approachable prices, the most varied housing stock in the area, and strong compatibility with VA, FHA, USDA, and Georgia Dream financing. This month's narrower asking-to-sold gap means fewer deep discounts, but also less frustration chasing overpriced listings, since inventory is priced closer to reality. Mortgage rates in the mid-6 percent range are a headwind but are stable and below last year. The one extra step in Byron is to run the Peach County tax math, and as always the right timing depends on your finances, timeline, and goals, best reviewed with a licensed agent and lender.

Q: Is now a good time to sell a home in Byron, GA?

A: Yes, provided you price realistically, which June clearly rewarded. Sellers who brought asking prices down closed the gap to sold prices and cut the sold pace from 64 days to 48. In the sub-$310,000 value core, a well-priced home in good condition should move at a healthy pace. The main risk is reverting to a high asking price, which is what left homes sitting earlier in the year, since Byron buyers are value-focused and will pass over an overpriced listing. Above $400,000, price sharply, because that end of the Byron market is thin and selective.

Q: Does living in Byron mean a longer commute to Robins Air Force Base?

A: Byron sits on the Interstate 75 corridor on the western side of the Middle Georgia market, so a commute to Robins Air Force Base or Warner Robins is longer than from the Houston County suburbs, but the highway access keeps it manageable, and many Byron buyers make that trade deliberately in exchange for lower prices. Byron also offers quick access toward Macon, which broadens its appeal to commuters working in multiple directions. For buyers whose main tie is to the base, the commute is a real consideration to weigh against Byron's affordability and its Peach County tax picture.

Q: Should I price my Byron home at the asking-price median or the sold-price median?

A: Price to the sold-price median for your specific band and neighborhood. This month the two are already close, an asking median of $298,877 against a sold median of $293,000, which reflects sellers recalibrating to reality and is exactly why homes sold faster. Reverting to a high asking price is the main mistake to avoid, since Byron buyers are value-focused and have a varied set of alternatives, and an overpriced listing will sit past the 68-day active average. Anchoring to recent sold comparables is what produced June's quicker sales and is what will produce a timely sale near full value.

About the Author

William Walton-Dean is a licensed REALTOR® with Walton Dean Realty, operating under Century 21 Homes and Investments, serving buyers and sellers across Houston County, Georgia, including Perry, Warner Robins, Bonaire, Kathleen, Byron, and the surrounding Middle Georgia housing market. Known for a data-driven, hyper-local approach and deep expertise in the military and PCS relocation market around Robins Air Force Base, he helps buyers and sellers at every price point make clear, confident decisions backed by real market insight.

📱 478-371-7069

Walton Dean Realty | Century 21 Homes and Investments

Buying or Selling With All This New Construction in Houston County? Let's Talk

New construction changes the math on both sides of a deal, giving buyers leverage and putting resale sellers in direct competition with brand-new homes. If you are buying or selling in Warner Robins, Perry, Bonaire, Kathleen, Byron, or anywhere in Houston County, Georgia, and want a REALTOR who tracks which builders and corridors are strong and which are overbuilding, reach out. Turning the new-construction landscape into a clear plan for your specific home, neighborhood, and timeline is what I do for every client.

William Walton-Dean | Walton Dean Realty

📱 478-371-7069

A More Strategic Approach to Real Estate

This information is provided for general educational purposes regarding new construction and the Houston County, Georgia real estate market. It is not financial, legal, tax, or investment advice, nor an endorsement of any builder. Community lineups, floor plans, incentives, and prices change frequently and should be verified directly with builders and a licensed real estate professional. Buyers and sellers should confirm current details for their specific situation.